Every 0.01% in concluded private equity transactions as a percentage of African GDP of $2.1 trillion, translates to more than $200 million of desperately needed incremental annual investment in the continent. This is according to a recent report by the Economist Corporate Network (ECN) on the trends and outcomes of private equity in Africa. Private equity investment in the region has grown significantly since the 1990s, when a handful of development finance institutions began investing in government-led development projects in Africa.

Today, about 140 private equity general partners are active on the continent. More than 1 000 private equity deals were concluded between 2010 and 2016 totalling $25.6 billion, according to data from the African Venture Capital Association (AVCA) and Prequin, which provides data for the alternatives industry.

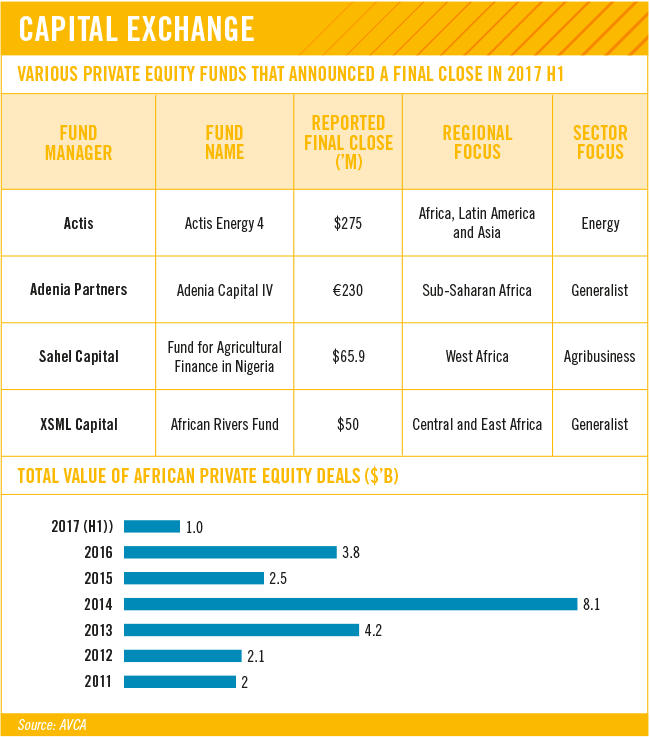

The years 2014 to 2015 saw, for the first time, capital raising of in excess of $7 billion for investment in Africa. During this time, Helios became the first private equity investor focused on sub-Saharan Africa to raise more than $1 billion, in its Helios Investors III fund.

‘We now have seen strong and sustained private equity investment in Africa over the past 10 years … as the region becomes more widely recognised as the world’s most exciting and attractive frontier investment destination,’ says AVCA CEO Michelle Kathryn Essomé.

According to the Washington-based Emerging Markets Private Equity Association (EMPEA), ‘some of the world’s largest alternatives managers have begun investing in sub-Saharan African companies, and their choice of targets points to a broadening and deepening of the opportunities available to investors’.

This includes the likes of the Carlyle Group, which raised $698 million for its first sub-Saharan Africa fund in 2014. Carlyle also led a group that invested $210 million in Tanzania-based Export Trading Group in 2012 and nearly $100 million in Mozambique-based J&J Africa in 2014. Another large player, Kohlberg Kravis Roberts & Co invested $200 million in Afriflora, one of the world’s largest rose growers, based in Ethiopia. Yet private equity investments are still small compared to other regions. Last year, private equity investment made up just 0.18% of Africa’s nominal GDP.

‘There are exceptions within the region, such as South Africa. However, a case may be made that the full potential of the asset class has yet to be realised, even there,’ states the ECN.

Pension funds in 10 African countries have an estimated $379 billion of assets under management, of which $29 billion could potentially be directed into private equity, according to the EMPEA. Some countries, including SA, Nigeria, Namibia and Kenya, have introduced pension fund reforms to encourage African institutions to invest more in private equity.

In developed markets, pension funds typically allocate around 5% to the asset class, but even a conservative 1% allocation would mean $3 billion could be invested in private equity annually by local pension funds, says Essomé. The AVCA sees African institutions playing a greater role in the growth of private equity. This year, Yeleen Capital reached a €30 million first close with capital raised solely from local institutions such as BOAD, the government pension fund of Côte d’Ivoire and insurance firm SONAVIE Mali, she says.

‘We are seeing a gradual rise in participation in the asset class from local pension funds, such as Eskom Pension and Provident Fund and Botswana Public Officers, but there is room for a lot more given the level of involvement so far,’ she says.

The Southern African Venture Capital and Private Equity Association (SAVCA) maintains that even in SA, private equity allocations are slower than more developed markets. But allocations are improving.

Tanya van Lill, SAVCA CEO, says pension and endowment funds accounted for 40% of all third-party funds raised during 2016. This was up from 35% in 2015. However, many pension funds were unfamiliar with the asset class. Also, large global investors may shy away from the region because the deals tend to be too small for them.

Just five African economies had GDPs of more than $100 billion in 2016, meaning large deals are ‘few and far between’, according to the Economist Intelligence Unit. Research shows that private equity funds have record levels of ‘dry powder’ – or money in search of deals, as managers battle to find the right opportunities.

Given the shortage of big deals, the next wave of African private equity will need to invest in the middle market, in the 10 000-plus companies with revenues of $10 million to $100 million, says Aubrey Hruby, co-founder of the Africa Expert Network.

With the exception of SA, African capital markets are fairly shallow. So private equity offers a different opportunity to tap the continent’s growth story in ways that cannot be accessed through capital markets. Despite some headwinds, including lower commodity prices, the African growth story is still compelling. The continent offers a growing middle class, rapid urbanisation and increasing consumerism.

At the same time, it’s becoming easier to do business in many African countries. Last year, 37 countries in sub-Saharan Africa adopted a record number of reforms (80) to make it easier to do business, says the World Bank Group’s annual Ease of Doing Business report.

Africa can really benefit from private equity, which tends to play a ‘catalytic role’ in economies, says the Economist. At the same time, investors earn decent returns. Between 2007 and 2015, ‘investors generated an average return well over 150% of the MSCI Emerging Market Index’, states the ECN.

African private equity outperformed the public markets by about 3% over the past three to five years, says Essomé.

The general shallowness of African capital markets and the high cost of debt finance mean that private equity plays an important role in helping to unlock and grow the potential of individual companies and ecosystems, according to the Economist.

Private equity investments in Africa tend to work differently to other parts of the world, where deals are associated with aggressive cost-cutting, increasing debt levels and exiting the business as soon as the investor can make a decent return.

In Africa, however, investors focus on growing businesses, building up the management teams, improving governance and strategy, and expanding supply chains.

Growth and job creation are priorities, and investors often scale businesses into large, viable concerns they can sell to trade buyers – competitors in the same industry – or larger private equity investors looking for bigger deals.

Van Lill argues that private equity investment results in more sustainable business practices and positive community outcomes.

‘Private equity plays a vital role in corporate governance, job creation, employment equity initiatives, skills programmes and social upliftment, thus rendering the portfolio company more resilient, more efficient, with healthier governance structures and with an expanded footprint,’ she says.

All in all, private equity helps build a sustainable, robust business sector, which is vital in growing African economies. Job creation is critical for the continent’s rapid urbanisation and increasing youth population. The AVCA measures the sustainability impact of private equity through job creation. In a survey of close to 25% of African private equity investors, it found that between 2009 and 2015, they grew their employment numbers by more than 17%. As an example, one of Actis’ SA-based investments, Food Lover’s Market, is adding an average of five new employees daily, says the ECN.

Southern Africa, largely led by SA, tends to attract the most private equity transactions – around 30% of completed transactions between 2010 and 2016, according to the AVCA.

West Africa, particularly Nigeria and Ghana, has attracted interest over the years, receiving one-quarter of private equity investment during the same time period. However, as Nigeria has been in recession and hard-hit by the commodity price drop, East Africa has become more of a focus for investors, particularly Kenya. From 2010 to 2016, East Africa attracted 18% of the equity deals, although the value of the deals tends to be relatively small compared to Nigeria.

‘In the short term, in the next 12 to 24 months, East Africa is certainly more appealing than West Africa,’ Natalie Kolbe, head of private equity for Actis, told the Financial Times in June. She said this was largely due to the instability of the Nigerian currency. North Africa attracted 15% of the total number of deals in Africa from 2010 to 2016.

The AVCA expects to see ‘a growing appetite in the most underserved markets, such as Central Africa. North Africa may also continue accounting for an increasing share of PE activity, as the region returns to political stability’.

The continent has experienced two ‘waves’ of private equity – the first involving large transactions in energy, natural resources and financial services; the second cashed in on consumers, focusing on healthcare, education and fast-moving consumer goods. ‘The industry is now on the cusp of a third wave that will incorporate the progress made during the prior waves and create value by focusing on the ligaments and tendons that hold together the economy and make it move,’ according to the EMPEA.

Construction, renewable energy, logistics, warehouses and mobile money platforms all fall into this so-called third wave. The EMPEA says these types of transactions are expected to give investors the returns they hope to achieve, but will also ‘advance the development goals of African countries by growing the sectors that make economies run more smoothly and supporting

the creation of desperately needed jobs’.

Agroprocessing, construction and infrastructure are expected to attract interest over the next five-year period, the EMPEA forecasts.

Private investment will also play a key role in e-commerce, renewable energy, education and the health sector. The continent has already seen some big deals in these areas. Actis, for example, invested $275 million in a higher-education platform across nine countries.

Considering the lack of employment in Africa, the continent needs to create jobs, particularly for youths, says Hruby. With a population of nearly 1.2 billion, more than 60% are under the age of 24, while youth unemployment across sub-Saharan Africa averaged 11% in 2016, she says, adding that a ‘tried and tested’ way to create jobs is through industrialisation and manufacturing.

The ECN describes private equity as ‘both a bridge to and engine of sustainable commercial development’ in Africa. As the benefits of private equity create win-win scenarios for both investors and society, the asset class is expected to continue to grow and thrive across the region.